{kind=link}

{kind=link}

The GST Council now plans to reduce the rate on real estate to 5% percent. A decision on this front is expected today

2017 is best remembered for ushering in a regulatory mechanism into the realty sector, especially with the passage of Real Estate (Regulation & Development) Act, 2016 and the new tax regime: Goods & Services Tax (GST).

What is GST?

It replaced a plethora of age-old 17 central and state taxes and 26 cesses. GST was seen as a tax that would liberate the taxpayer from the evils of cascading, a multiplicity of the levy, unwarranted litigation, compliance burden, among others.

Read Also: material under 5% GST slab, says PM Govt wants to bring construction Modi

Real estate and GST

One sector that was looking up to GST as a panacea for all its tax woes was real estate. It expected GST to provide some impetus to the sector by liberating it from hidden taxes, black money, multiple assessments, audits and tax procedures. GST was expected to make the paradigm shift from favouritism to transparency and from discretionary administration to a policy and system-based administration.

GST and immediate impact

Regulations imposed by the government to ensure accountability on the developer such as the Real Estate (Regulations and Development) Act, 2016 (RERA); Goods & Services Tax Act; and the Benami Transactions (Prohibition) Amendment Act, 2016 all discouraged speculators and laid the foundation of a healthy end-user market In the last two years since its introduction, GST has been a major factor keeping homebuyers away from under construction apartments. Many developers are now willing to absorb most of the GST impact on buyers in under-construction projects to boost sales, particularly in the low-ticket size apartments and in the affordable segment.

GST and under-construction properties

Currently, GST is levied at an effective rate of 12 percent (standard rate of 18 percent less a deduction of six percent as land value) on premium housing and effective rate of eight percent (concessional rate of 12 percent less a deduction of four percent as land value) on affordable housing on payments made for under-construction property or ready-to-move-in flats where completion certificate has not been issued at the time of sale. However, GST is not levied on buyers of real estate properties for which completion certificate has been issued at the time of sale.

The GST Council now plans to reduce this rate, with many anticipating it to be reduced to five percent. A decision on this front is expected on January 10.

“If the government reduces the eight percent GST rate on affordable housing to five percent without extending the benefit of the input tax credit, sale prices may increase and real estate developers may pass on the burden/increase in the price of apartments for most low and middle-income projects. This may impact the government’s affordable housing scheme,” said Harpreet Singh, Partner, KPMG.

Read Also : GST Council to meet on Jan 10; to consider 5% GST on under-construction flats

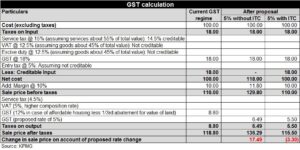

The same can be explained with the following illustration:

In case of affordable housing, sale price could see an increase (by Rs 17.49 on every Rs 100 in the above example) in case the GST rate is reduced to five percent from eight percent on account of denial of the input tax credit. However, if the rate is cut to five percent from eight percent while allowing input tax credit, prices could reduce (by Rs 3.3 on every Rs 100 in the above example)

Prior to the GST rollout, under-construction housing projects attracted 4.5 percent service tax and a value-added tax (VAT) of 1-5 percent depending on the state. Also, inputs used in construction attracted 12.5 percent excise duty in addition to 12.5-14.5 percent VAT. Besides, the entry tax was also levied on inputs.

After adjusting for credits on inputs used, the effective per-GST tax incidence on such housing property was 15-18 percent.

What do real estate developers want?

Builders are hoping that the government will allow input tax credit on under-construction residential properties even after reducing the GST rate to five percent.

“We are quite optimistic about the revision of GST rates on residential properties. However, National Real Estate Development Council (NAREDCO) wishes for an input tax credit, as the absence of the same will lead to a steep rise in price, which will majorly impact the affordable segment, thus directly affecting the central government’s dream of Housing for All by 2022. We are looking forward for a 12 percent tax bracket, with abetment of 50 percent for land cost and other premiums, effectively bringing the tax rate at six percent with input tax credit. We are also expecting a revision on GST as it will largely help in converting the fence-sitters into buyers,” said Rajan Bandelkar, President, NAREDCO West.

“GST reduction is a very good move but the only request is that input tax credit should not be withdrawn. If it is withdrawn, the cost of burden of input tax credit will get passed on to customer, thereby increasing his cost of acquisition. Reducing it to five percent with input tax credit is brilliant. It will be a shot in the arm for the real estate sector, especially affordable housing. With income tax credit it should come down to five percent, otherwise it should stay at eight percent,” said Joyville Shapoorji Housing, Managing Director, Sriram Mahadevan.

GST, input tax credit and homebuyers

While the overall cost of construction seems to have fallen under the GST regime on account of additional input tax credits for builders, the intent to pass on the benefit of lower cost of construction to the end-buyer appears to be still missing in the market.

Read Also : Why reduced GST will prove costly for budget homebuyers

The Finance Ministry has time and again asked real estate dealers to pass on GST rate cut benefits to home buyers but to no avail.

In order to ensure that the benefits reach the ultimate buyers, the Centre in December 2018 started questioning the developers/builders who were not passing on the benefit of reduced rates and additional input tax credit by triggering anti-profiteering measures.

It clarified that homebuyers of real estate properties will not have to pay GST if they purchase a fully constructed property after the issue of completion certificate. It has also asked builders to reduce prices of properties by passing on the benefit of a lower GST rate.

The government’s note in December 2018 appeared to be an outcome of anti-profiteering complaints against some builders, after it was brought to its notice that some builders/contractors are not passing on the benefit of lower tax burden to homebuyers.

GST and ready-to-move-in properties

One of the benefits and the major attractions of ready-to-move-in properties is that they are exempt from GST, provided that the project has been issued a completion certificate. Buyers of such properties need to pay only the stamp duty and registration charges as taxes, which comprise 7-8 percent of the total property cost. A survey by ANAROCK had highlighted that buyer preferences are significantly skewed towards ready-to-move-in properties. Over 49 percent of today’s property seekers prefer to buy ready properties to save on costs, avoid project delays and unscrupulous builders.

GST and affordable housing

In a major push to the affordable housing segment, the government also extended the GST benefit to its Credit Linked Subsidy Scheme (CLSS) for economically weaker sections (EWS), lower income group (LIG), middle income group I (MIG-I) and MIG-II homebuyers. Besides receiving interest subsidy, buyers can also avail of a lower concessional GST rate (8 percent).

To boost sales in this segment, the government had urged developers to refrain from charging GST from homebuyers as the effective eight percent GST rate can be adjusted against their input credit should they opt for this.

The Centre also recognised the need to promote real estate sector to the weaker income group and accordingly extended the concessional rate (12 percent) for construction of houses under CLSS to promote affordable housing for EWS, LIG and specified middle income groups. The effective GST rate for such projects further comes down to eight percent after deducting one-third of the amount charged for the house/flat towards land cost.

Have expectations been met?

GST has undoubtedly assisted in formalisation of the sector to some extent. Not obtaining GST registration and evading tax by remaining outside the tax net is no more a lucrative option. It makes sense for stakeholders like suppliers of building material, works contractor etc to register themselves and avail benefit of input tax credits.

As a large majority of goods used in the real estate and construction segment were sourced from vendors operating in the unorganised space, benefit of availing input tax credit at each stage has encouraged them to come within the tax ambit.

GST has been successful in liberating the sector from multiple levies like excise and VAT on manufacture/procurement of goods (cement, steel, bricks etc); service tax on construction, engineering, brokerage, architecture, et al; and entry tax on bringing construction material within a state etc. With GST subsuming these taxes, there is only one tax to be paid.

Also, it was expected that removal of cascading effect of taxes (tax over tax), availability of additional input tax credits and decreased logistic cost on account of reconfiguration of supply chain under GST was expected to reduce overall construction cost.

Tax optimisation has driven structuring of entities and contracts may not be required under GST. Under the erstwhile tax regime, with VAT applicable on goods and Service Tax on services, there was a tendency to split construction contracts into material and service portions to optimise taxes. With the advent of GST, the need to split the contract into material and service portions would not arise as the entire works contract (in relation to immovable property) would be treated as services liable at 18 percent (i.e. effective rate of 12 percent after claiming one-third deduction for land for premium housing), Singh said.

GST – a work in progress

Issues like ambiguity on treatment of Joint Development Agreements (JDA), taxability of Transfer of Development Rights (TDRs), restriction on availability of credit in case of works contracts resulting into immovable property (other than to contractor), allowing centralised registration etc still need to be addressed under GST.